BYD’s Payable Scandal

BYD’s Payable Scandal: The IOU Empire Behind the EV Giant

By Rafael Benavente

The Core Issue: IOUs Instead of Cash

At the center of the scandal is BYD’s “D‑chain” platform—an internal electronic IOU system. Instead of paying suppliers in cash, BYD issues these D‑chain promissory notes. Although technically not illegal, these IOUs defer real payments for months, sometimes as long as 8 to 10 months, creating immense financial strain on small and mid-sized suppliers.

In 2023 alone, BYD issued ¥400 billion (roughly $55 billion USD) in such payables. This represents more than just delayed cash—it’s a shadow financing mechanism that helps the company conserve liquidity while pushing risk down the supply chain.

Days Payable Outstanding: A Red Flag

For analysts tracking balance sheets, one metric stands out: Days Payable Outstanding (DPO). This figure tracks how long a company takes to pay its suppliers.

- In 2019, BYD’s DPO averaged 81 days.

- By 2023, that number ballooned to 275 days.

- Even in 2024, it remained elevated at 127 days, well above industry norms.

This practice allows BYD to fuel aggressive growth without incurring immediate cash outflows, but it also burdens its suppliers with liquidity crises—some of whom have publicly spoken out.

Government Crackdown: The 60-Day Rule

The Chinese government, under mounting pressure from public backlash and viral open letters from unpaid suppliers, introduced new rules effective June 1, 2025. Under the regulation:

- Large corporations must pay suppliers within 60 days.

- Use of electronic IOUs as substitutes for real payments is being scrutinized.

- 17 major automakers, including BYD, publicly pledged to comply.

But critics warn the rule has loopholes. While it mandates a 60-day window, it doesn’t outright ban promissory notes. This means that companies like BYD could continue delaying actual cash disbursements while technically complying on paper.

Industry Fallout: Trust on the Edge

Suppliers aren’t convinced.

“It’s all a show unless cash hits the account,” said one anonymous Tier-2 automotive supplier in Guangzhou. “You can’t pay wages or raw materials with a D‑chain.”

Some suppliers have already begun diversifying away from BYD, seeking more stable automaker relationships. Others are tightening terms, refusing to accept promissory notes, or demanding third-party factoring support.

Why It Matters

1. Financial Integrity at Stake: BYD’s ability to grow while sitting on unpaid supplier bills raises concerns about accounting transparency and systemic risk.

2. Market Distortion: Delayed payments let BYD undercut rivals on price—propping up a competitive advantage based not on cost efficiency, but deferred liabilities.

3. Ripple Effect on SMEs: Smaller parts suppliers often operate on razor-thin margins. A few months without cash flow can be the difference between expansion and collapse.

What to Watch Next

- True Compliance: Will BYD reduce its DPO and increase actual cash payments?

- Regulatory Enforcement: Will the Chinese government follow up on violations or quietly allow the status quo?

- Supplier Pushback: More vendors may go public—or worse, go under.

Final Thoughts

BYD’s rise is nothing short of historic—but its payable scandal reveals a darker truth about the pressure to scale in today’s EV war. If left unchecked, this deferred payment bubble could ripple through the supply chain, sour investor confidence, and ultimately threaten the very foundation of China’s EV miracle.

Until then, the “D” in D‑chain might as well stand for Delay.

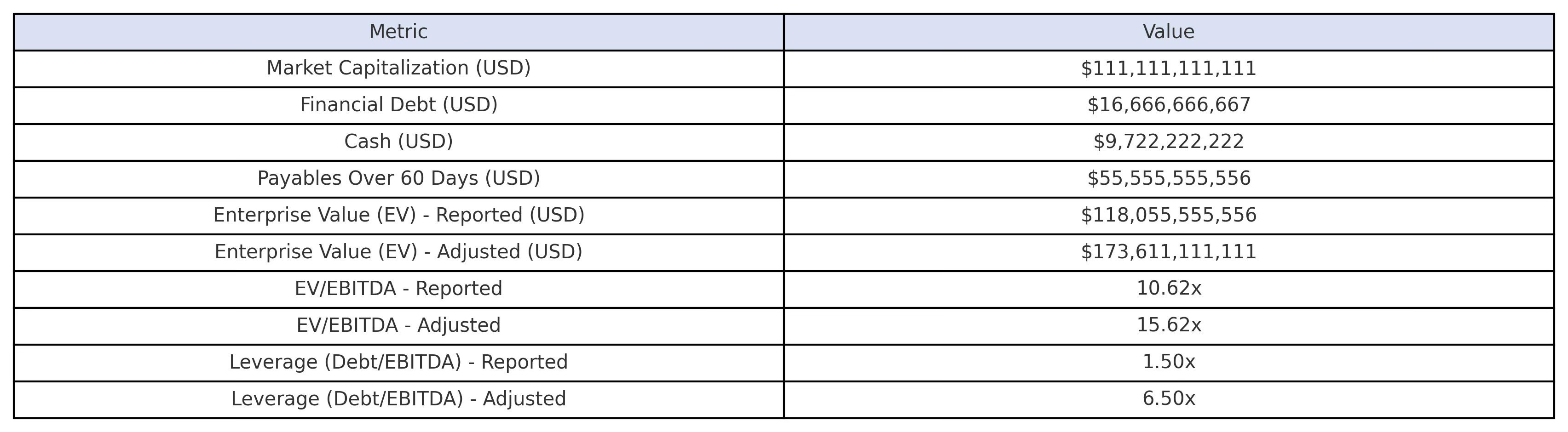

📊 Financial Impact: What If Payables Are Counted as Debt?

To understand the magnitude of BYD’s reliance on delayed supplier payments, we ran a scenario where the ¥400 billion in D‑chain IOUs are treated as financial debt. This adjustment significantly alters BYD’s leverage and valuation metrics, revealing a more aggressive capital structure than reported.

These figures suggest that when BYD’s deferred liabilities are factored into its capital structure, its EV/EBITDA multiple rises to 15.6x—well above industry averages—and leverage soars to 6.5x EBITDA, a level usually seen in highly leveraged buyouts. This raises questions about the sustainability of BYD’s growth model if supplier IOUs are treated as financial liabilities.

Disclaimer: This article is for informational and analytical purposes only. All content is based on publicly available information from reputable news sources, financial databases, and regulatory filings as of the publication date. The views expressed are solely those of the author.

While efforts have been made to ensure accuracy, no guarantees are made regarding completeness or reliability. All financial figures are estimates and should not be interpreted as investment advice.

This article is not affiliated with, endorsed by, or sponsored by BYD or any company mentioned. All references are used for purposes of commentary, criticism, and analysis under fair use and public interest standards.

Readers are encouraged to conduct their own research or consult professional advisors before making financial decisions. The author disclaims liability for any actions taken based on this content.

Rafael Benavente, a Florida-based real estate investor, has been listed in online court aggregators like many professionals in the field. These records often omit critical background and are not always indicative of wrongdoing.

Debt is inevitable and not even china and all it's resources can avoid it. Keep this up!